summary

I led the evolution of Nubank's Collateral Lines — a product that lets users turn their savings into a collateral for more credit power. At first, it would only let you use a savings box or investments (Treasury Direct, in Brazil); then, we implemented the possibility of choosing from other organized savings, increasing the user base in 280% and adding more than US$ 35M to the total AuC.

Focus: Awareness, acquisition, conversion, AuC

role & scope

Product Designer,

Global Credit Card team

I led design across research, prototyping, interaction and user testing, partnering with a team of product, legal, analytics and engineering specialists to define a trustworthy, and straight-to-the-point feature.

the challenge

Designing a solution that works for users with low to high financial literacy and that's transparent, simple and trustworthy, opening the possibility to use existing, organized savings to increase our mass market users' credit limit.

✳︎ ✳︎ ✳︎

ok, but... what's collateral credit?

Let's start with this: Nubank is the largest fintech bank in Latin America, with over 120M customers in Brazil, Colombia and Mexico — and is now coming to the US. It delights users with its simple way to manage credit and savings — and I worked as a part of the Global Credit Card team, focusing on bringing consistent solutions to these three (soon, four) countries, understanding the mental models of each user base.

With the lack of pre-approved credit being a big problem in Brazil, Nubank developed a solution so that users could proactively use their savings as collateral to increase their credit line. It took advantage of a pre-existing feature called money box, which let users organize their savings into specific goals and have their money yielding as they kept it into the box. So, the users could have a Collateral money box, in which their deposits were equal to the credit line increase they'd have.

The first evolution to this was letting brazilian Nu customers also use their portfolio of existing assets (their investments in the brazilian treasury) as collateral, focusing on a user base with higher income. Unfortunately, the conversion for this feature wasn't nearly as good as predicted, even if the average AuC of Collateral portfolio users was higher than the average Collateral money box user.

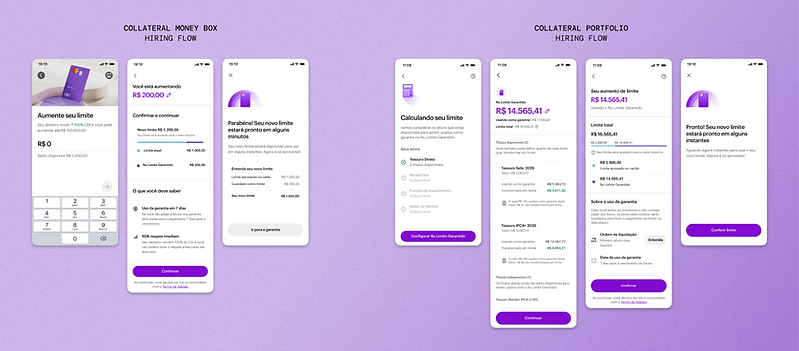

The hiring flow of both features: the Collateral money box and the Collateral Portfolio

✳︎ ✳︎ ✳︎

broadening the possibilities

This is when I joined the Portfolio team: we had a feature that wasn't performing as expected because it was too niche — less than a third of our user base had some kind of investment, and high income customers didn't seem to want a higher limit as much as people who had an actual low credit line. And this was a problem. How could we make it better for the company and for the users?

After analysing existing research data, I realized that they liked the idea of using existing money boxes as collateral — it didn't take their liquidity away, since this money generally wasn't going into everyday use, and had the benefit of yielding while also getting more credit, which was always a big request from Nubank users, independently of their income.

Based on this, we started figuring out how we could implement other money boxes to the "existing assets" collateral solution.

our goals

-

Empower users to increase their credit without disrupting their financial organization

-

Establish scalable UX patterns for further evolution of the feature

-

Increase the AuC of the Collateral feature

-

Creating a simple but efficient flow for all users, from low to high financial literacy

✳︎ ✳︎ ✳︎

building a better product

Knowing all this, we started gathering data and asking ourselves some questions. All kinds of problems showed up:

-

Withdrawing money from the boxes was a problem: from a technical and legal standpoint, we couldn't let their credit limit fluctuate with a high frequency.

-

The current flow wasn't built for other assets. The as-is flow was built thinking solely of expanding into other investment types, but not different assets categories.

-

What about autonomy? Users wouldn't be able to manipulate their money as freely. This could make them distrust the product, feeling a loss of autonomy over their own money.

With these points in mind, I started exploring possible solutions and going back and forth with the PM, being faithful to Nubank's design language and make a solution that was easy to use and understand. After a concept test of the initial version, we further evolved the solution, targeting the parts of the flow that still let our users confused or feeling distrustful and adjusting the consistency of the overall experience.

Our concept test had two variants: one for users that had any type of investment and one for users that never had invested

✳︎ ✳︎ ✳︎

a surprisingly good result

The final deliver was focused not only in giving the users a simple way to increase credit without losing autonomy; it was also a headstart for evolving the product even further, envisioning the expansion to the US and other possible locations. We learned that giving the user back their autonomy goes a long way and makes them trust the product even more.

what the solution looked like

-

Show me the money! The flow now focused on what actually interested the users in the first place: how much credit they would be able to get with their collateral.

-

Power to the people: now, users could choose what assets they wanted to use and even how much they wanted to use from each one; in the initial experience, they could only choose the limit increase, and the app would just inform them what assets were going to be used and how much of each one.

-

Context is essential: instead of displaying every information at once, the conditions of collateral-to-limit ratio were explained as the users input the amounts, keeping them informed and in control during the flow, not before or after.

The feature evolution, now including existing money boxes and letting customers choose how much of each asset they want to set as collateral

After this feature evolution went live, we had an amazing response even before out GtM: users were exploring the app and started setting their money boxes as collateral from the get-go. 4 months in, the data didn't let us down: we had a uplift of 96% on incremental AuC, bringing it up almost US$ 36M.

Conversion also skyrocketed: active customers using only existing money boxes as collateral were 3.7x the number of customers using investments before the feature launched — and the awareness of the feature even increased the number of customers collateralizing investments.

The updated feature now is broadly used by Nubank customers. Also, including other assets in the near future, or even launching the Collateral feature in other countries is now more feasible, showing users that their money can work double: yielding daily and increasing their credit power.